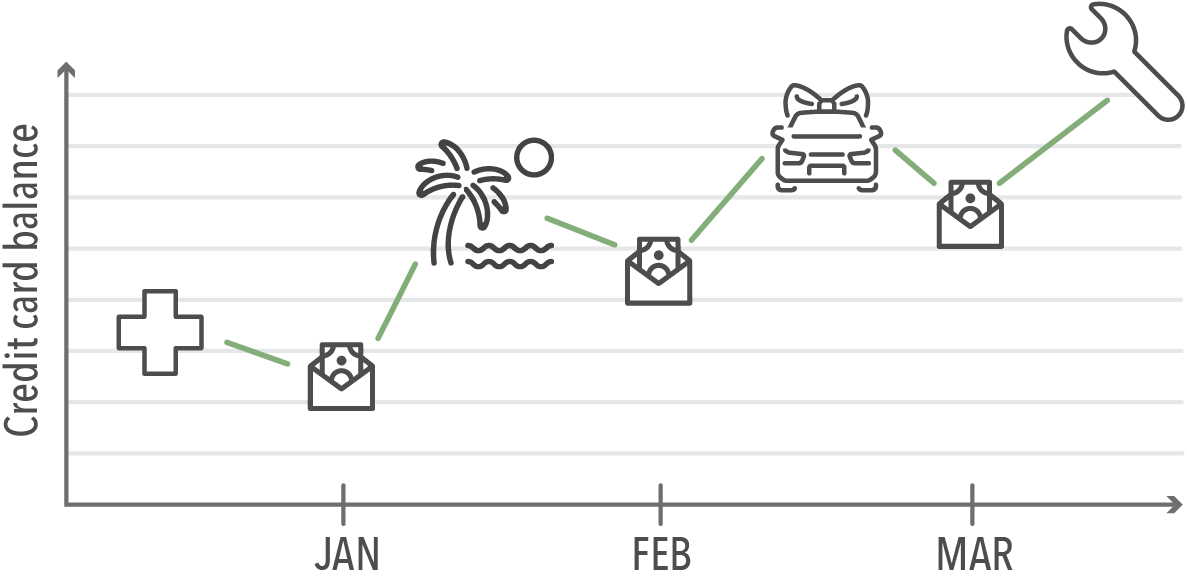

The Debt Cycle

Here’s how it happens:

- An event usually triggers the cycle, such as a healthcare emergency, expensive home or car repair, major purchase, or planned vacation.

- You intend to pay off the debt quickly.

- The debt doesn’t get paid off as planned due to reasons and circumstances.

- You make monthly payments, but keep adding new charges.

- You make larger payments when you can, but new charges continue to increase the balance, never allowing you to substantively reduce the balance or get it to zero.

- As the balance builds, your tolerance for debt grows.

- In extreme cases, the balance builds until the credit line is maxed out and you must find a new source of credit.

The most common way this occurs is using credit cards or bank overdraft lines of credit.

Bank overdraft protection

When you are approved for overdraft protection on your checking account, it can save you the cost of overdraft fees and the embarrassment of a declined purchase.

However, if charges pile up, you may tend to bring your negative account balance back to positive on payday and then make new purchases on the freshly cleared line of credit. This process can incur high fees and finance charges and could trap you in a debt cycle for months or years.

Credit cards

Most of us use credit cards with the intent of paying them off fully each month. When larger purchases pile up, it can be impossible to make the full payment as planned. You might make larger payments when you can, but if you keep using the card, you add to the balance and create a cycle of perpetual debt. The balance can grow until you feel overwhelmed and out of control.

Break the debt cycle

If this sounds familiar, find out how to break the debt cycle and become free from consumer debt here.